The

1960s

A decade of increasing independence during which a strategy

of vertical integration and horizontal diversification

in the product range is adopted.

1961

Nuclear Developments Ltd is formed. It is a consortium

of the Company, Rolls-Royce and Rio Tinto formed to manufacture

nuclear fuel elements.

1962

Metals Division and its subsidiaries (excluding the aluminium

interests) will henceforth be  grouped

within a new holding company, Imperial Metal Industries.

The operating company will be Imperial Metal Industries

(Kynoch) Ltd. The fifteen-year process of disengagement

from ICI has started.

grouped

within a new holding company, Imperial Metal Industries.

The operating company will be Imperial Metal Industries

(Kynoch) Ltd. The fifteen-year process of disengagement

from ICI has started.

At this time IMI (Kynoch) is the largest UK producer of

copper and copper alloy semis, particularly sheet. In

rod and section Delta is the main competitor. In strip,

Ratcliff (Great Bridge) is the major supplier. Profitability

is inadequate, partly due to the large, ICI-like overhead

structure and partly to under-utilisation of capacity.

The New Metals business, recently a major contributor

to profits, is about to suffer a severe downturn. In Ammunition

and Metal Fabrication profits are negligible due to depressed

prices and high costs.

A large electron beam furnace is on order intended for refractory metals such as niobium and tantalum.

J. F. Ratcliff (Metals), a Birmingham manufacturer of

copper and brass sheet and strip, is acquired.

intended for refractory metals such as niobium and tantalum.

J. F. Ratcliff (Metals), a Birmingham manufacturer of

copper and brass sheet and strip, is acquired.

A commemorative book marking the Company's 100th anniversary

is published by The Kynoch Press - "Under Five Flags"

(which have now become six). The author, who is unacknowledged

at the time, is Dorothy Thomas, an employee.

1963

Imperial Metal Services is formed. Its purpose is to acquire

shares and other interests in companies dealing in metals.

Henry Righton (a merchant of copper semis) is acquired

for £1m. A small stake is taken in Range Boilers.

Talks about future cooperation are held with BICC but

no attractive case for a merger of interests appears.

This is the end of moves towards horizontal integration

for some years.

1964

In a drive towards rationalisation and greater  efficiency,

Steatite and Porcelain is sold to Morgan Crucible Ltd.

and the Elliott Works at Selly Oak is also disposed of.

Opti Group and Lightning Fasteners are in talks about

future cooperation which will lead to a merging of their

interests in the following year. Range Boilers (right)

and the Company enter a cooperative arrangement. The Company

takes advertising space to clarify the position regarding

high copper prices and supply shortages. The modernised

strip mill at Witton (below) is formally

opened. A 29% stake is taken in Wolverhampton Metal (Holdings).

efficiency,

Steatite and Porcelain is sold to Morgan Crucible Ltd.

and the Elliott Works at Selly Oak is also disposed of.

Opti Group and Lightning Fasteners are in talks about

future cooperation which will lead to a merging of their

interests in the following year. Range Boilers (right)

and the Company enter a cooperative arrangement. The Company

takes advertising space to clarify the position regarding

high copper prices and supply shortages. The modernised

strip mill at Witton (below) is formally

opened. A 29% stake is taken in Wolverhampton Metal (Holdings).

1965

A new facility to manufacture waterproof sporting ammunition

- an important innovation - is opened by a former chairman,

Dr. Beeching. The Company is the world's biggest exporter

of sporting ammunition with 40% of its output going abroad,

this year 38,400,000 cartridges. Powder and Shot,

a documentary about gun construction and markmanship,

made by the ICI Film Unit for the Company, is issued.

1965

A new facility to manufacture waterproof sporting ammunition

- an important innovation - is opened by a former chairman,

Dr. Beeching. The Company is the world's biggest exporter

of sporting ammunition with 40% of its output going abroad,

this year 38,400,000 cartridges. Powder and Shot,

a documentary about gun construction and markmanship,

made by the ICI Film Unit for the Company, is issued.

A

merger occurs between Lightning Fasteners and the Opti

Group. YKK, a serious Japanese competitor, opens its first

European factory in Holland.

A successful bid is made to acquire Range Boilers. This

move coincides with a spate of company prestige advertising:

"My My My....IMI".

1966 IMI becomes a public company: an issue of

Imperial Metals Industries Loan Stock is announced and

of 10m. Ordinary Shares. ICI still holds 89.6% of the

stock but this is widely seen as a move by ICI to grant

its subsidiary greater independence. The equity offer

is heavily oversubscribed.

John Wilkinson and Sons (Saltley), makers of copper alloy

strip and wire, is acquired together with its subsidiary

Headley, Birch & Co. Santon Ltd of Newport (electric

water heaters) is also acquired. Annual profits are £6.4m

1967

The titanium interests of Jessop-Saville, Sheffield, are

to be acquired.  The

remainder of the equity in Wolverhampton Metal (Holdings)

comprising James Bridge Copper Works (left)

and Wolverhampton Metal Co. (both metal refiners) is also

bought. The move from paper to plastic sporting cartridge

cases is to be speeded up, to about 75% of the total of

the 100 different types manufactured. Amongst the latter

Tenex target ammunition sales now amount to 20m. units

a year. A new extrusion press in the Rod Mill is commissioned.

Company turnover is £77m. yielding a profit of £4.7m.

The

remainder of the equity in Wolverhampton Metal (Holdings)

comprising James Bridge Copper Works (left)

and Wolverhampton Metal Co. (both metal refiners) is also

bought. The move from paper to plastic sporting cartridge

cases is to be speeded up, to about 75% of the total of

the 100 different types manufactured. Amongst the latter

Tenex target ammunition sales now amount to 20m. units

a year. A new extrusion press in the Rod Mill is commissioned.

Company turnover is £77m. yielding a profit of £4.7m.

Dead Safe, a film on safety in shooting, is issued.

1968

An offer is made to buy Yorkshire Copper (Holdings), the

Company's partner in ownership of Yorkshire Imperial Metals

and is accepted.  The

Company launches a domestic tap made of plastic under

the trade name Opella. Yorkshire Imperial Plastics

starts to market an underground pvc drainage pipe (right,

in 1975). Rolls-Royce's Lockheed Airbus contract

is likely to lead to sales of 1500 tons of titanium. Much

new plant is commissioned: a high speed rolling mill for

copper and brass foil; new melting and casting facilities

for the strip and sheet mills; and a new liquid-metal-cooled

vacuum melting furnace for titanium. Turnover is £168m.

The

Company launches a domestic tap made of plastic under

the trade name Opella. Yorkshire Imperial Plastics

starts to market an underground pvc drainage pipe (right,

in 1975). Rolls-Royce's Lockheed Airbus contract

is likely to lead to sales of 1500 tons of titanium. Much

new plant is commissioned: a high speed rolling mill for

copper and brass foil; new melting and casting facilities

for the strip and sheet mills; and a new liquid-metal-cooled

vacuum melting furnace for titanium. Turnover is £168m.

1969

A 51% stake is acquired in

Paxman Cooler Manufacturing Co. of Brighouse (beverage

cooling and dispensing). An unsuccessful bid is made for

Enots, Lichfield (pneumatic control equipment). The Company

is in 78th place in a list of top British industrial companies

based on capital employed. In response to a survey the

Company states that the number of employees earning more

than £10k p.a. is "about 10". Henry Righton & Co.,

the Group's metal stockholding company, announces that

henceforth its pricing will be based on decimal currency

and metric measurements. A new company, I.M.I. Australia

Ltd., is formed to manage and expand the Company's metal

and ammunition interests in that country. Courtaulds and

ICI agree to cooperate in the field of composite materials;

Imperial Metal Industries will be involved.

Because of the issue of new shares to support acquisitions,

ICI's stake in the Company has now dropped to 65%

The

1970s

An unhappy decade with British industrial relations plumbing

new depths and foreign competition increasing but with

the Company obtaining full independence again after 60

years and still actively investing in new plant, continuing

to diversify into new product areas and establishing a

completely new business area of great future significance.

The advertising slogan is "IMI means more than metal".

1970

A new titanium rolling mill is ordered

for Waunarlwydd. Compression Joints Ltd. of Weston is

acquired.  The

Company commits itself to a multi-million pound expansion

of titanium capacity once Concorde reaches its performance

targets. The Company's Managing Director, St.John H. Elstub

(left),

is knighted. G. Brammall (Tungsten) is acquired as is

Clix Fastener Corporation of Montreal. Rolls-Royce collapses

but the Company consoles itself by putting the cost at

no more than £1.5m, borne mainly by IMI Titanium and Marston.

Winfield Metals, a small strip manufacturer is acquired;

but capital expenditure dwindles and IMI's Chairman publicly

questions for the first time the future of the UK semis

market.

The

Company commits itself to a multi-million pound expansion

of titanium capacity once Concorde reaches its performance

targets. The Company's Managing Director, St.John H. Elstub

(left),

is knighted. G. Brammall (Tungsten) is acquired as is

Clix Fastener Corporation of Montreal. Rolls-Royce collapses

but the Company consoles itself by putting the cost at

no more than £1.5m, borne mainly by IMI Titanium and Marston.

Winfield Metals, a small strip manufacturer is acquired;

but capital expenditure dwindles and IMI's Chairman publicly

questions for the first time the future of the UK semis

market.

1971

The national engineering workers'

strike against the Industrial Relations Bill closes Kynoch

Works for a day. After poor results Enots agrees to a

reduced bid from the Company. The quest for innovative

new products leads to the Company finding itself managing

a Scottish oyster hatchery. Profits are £14.17m helped

by cost cutting measures including a 1000 reduction in

staffing levels.

1972

350 maintenance workers strike over

a pay claim affecting the entire Witton site. The Company

is not alone: most of the British car industry is in chaos

due to industrial action. Builders' and miners' strikes

also affect the Company's activities.

Nevertheless innovation and acquisition continue. Marston

Radiators collaborate with two European firms to produce

the newly developed aluminium car radiator. The Company

has developed a revolutionary new lightweight domestic

boiler. IMI Engineering Plastics is created at Witton

to handle the design and production of new fibre-reinforced

materials. A surprise offer is made for Norgren Shipston

International and its US associate, C.A. Norgren (pneumatic

equipment). Muntz Plastics, Wrexham (plastic pipes and

fittings) is bought.

It is expected that IMI Titanium's sales will recover

from the Rolls-Royce disaster to a level equivalent to

that for 1970.

1973

Inflation is running at 24%. For

the Company, it is a year of disasters. Two Rolls-Royce

RB211 Tristar engines fail in flight. The cause is traced

to front fan discs manufactured from IMI Titanium forgings.

Investigation work is urgent and detailed and business

is affected. Even worse, an electric drill being used

by a maintenance engineer on a contaminated explosives

loading machine sparks off a major explosion at Witton

in the sporting ammunition area. Six

people lose their lives

and a further fifteen are injured, one seriously. A question

is asked in Parliament and at the inquest the Company

is criticised.

The Company forms with Olin Corp. a joint venture company,

Marstolin, to market coated titanium anodes for chlorine

and similar applications. Mecafrance (valves) is acquired

Turnover is £275m giving a profit of £14.9m.

1974

The country suffers from the chaos

of the three-day week resulting from industrial action

by the miners. The Company says that it is maintaining

output at 85% with the help of in-house generating capacity.

Witton is not immune from the general industrial anarchy.

On October 7th a strike over pay by 1000 craftsmen starts.

Production workers strike over layoffs caused by the strike.

On November 9th the craftsmen agree to resume work. Production

has been halted in the meantime and 5000 other employees laid

off. (10,000 are also idle at British Leyland). The strike

has cost the Company about £3m. YIM's performance causes

concern, affected by the poor industrial relations situation

at Kirkby. Trading conditions are in any case difficult

especially in building and textiles: 190 Lightning Fasteners

workers (left)

will lose their jobs because of Japanese competition and

the price of copper peaks at a level three times higher

than that of three years previously.

been halted in the meantime and 5000 other employees laid

off. (10,000 are also idle at British Leyland). The strike

has cost the Company about £3m. YIM's performance causes

concern, affected by the poor industrial relations situation

at Kirkby. Trading conditions are in any case difficult

especially in building and textiles: 190 Lightning Fasteners

workers (left)

will lose their jobs because of Japanese competition and

the price of copper peaks at a level three times higher

than that of three years previously.

Plans are announced for further expansion of the building

products area of activity in various plants throughout

the country. The Company agrees to buy the fine tube interests

of Serck Ltd.

Top Brass is released, a film showing how non-ferrous

rod and wire are produced.

1975

The Company protests at Japanese

dumping of fasteners. The adverse effect on business is

increasing. IMI Impala is sold. The Board considers a

proposal that due to all the difficulties of operating

in the UK 70% of all future acquisitions should be overseas.

"A drab and dispiriting year".

1976

A rights issue is announced, mainly

to finance a stake in a new Iranian copper semi-finished

products factory. This latter project however fails to

come to fruition. UK acquisitions will be made with the

aim of reducing dependence on copper-based activities.

The Company is operating a waste-burning boiler within

its 50mw power station. A protest is made at unfair Japanese

price-cutting of titanium products and the high tariff

wall protecting their suppliers. Against

the background of industrial turmoil in the West Midlands

a decision is made to move the IMI Opella operation off

the Witton site to the calmer waters of Hereford; despite

violent opposition this move eventually occurs.

1977

The Evening Mail contains

a blank column where a report on the Company's results

should have appeared, N.G.A. representatives having refused

to handle the information since it has been received by

telephone rather than the N.G.A. member manned teleprinter.

The Company buys Mapegaz-Remati, France (industrial valves).

IMI Valves International is formed to spearhead the growing

industrial valve activity. Exploratory talks with Delta

Enfield with the aim of rationalising rolled metals manufacture

and investment come to nothing. ICI sells off its 63%

stake in Imperial Metal Industries and the Company is

now independent for the first time since 1918.

1978

As

the Company relishes its independence and looks forward

to the future, it has 27,000 employees in the U.K., plus

a further 6000 overseas. 44% of its equity is owned by

private shareholders including many employees and pensioners.

Samuel Birkett, Yorkshire, (specialist

valves) is acquired as well as a majority stake in Whittaker

Hall (compressors and pumps). It is alleged that the 1974

Japanese commitment to reduce the export of YKK fasteners

to the U.K. has not been honoured. 40% of the market is

now in Japanese hands.

1979

The Company changes its name to

IMI. The "Imperial" tag is no longer appropriate

and the abandonment of "Metal", which no longer

accurately describes the company, is part of a strategy

to expand overseas

and into products with a higher added-value content.

overseas

and into products with a higher added-value content.

The possibility of cooperation with Delta is again thwarted.

The Kynoch Press is sold.

A new group is formed, IMI Drinks Dispense, comprising

Paxman and Redditch Controls and a new company is

established with Cornelius, USA. These moves are intended

to allow greater exploitation of the potental market for

drink dispensing equipment and are highly significant

as far as the Company's future is concerned.

IMI Norgren Shipston receives the Queen's Award for Export

Achievement (right).

The

1980s

In this decade which starts with a serious trade recession,

not helped by a lengthy strike in the steel industry,

the Company will move towards higher margin finished products

such as pipe, tubes and fittings and develop those new

areas of business on which its future will eventually

prove to depend. The traditional "metal-bashing" activities

will decline.

There is now clearer definition of the Company's main

activities. They fall currently within seven product groups:

Refined and Wrought Metals (the metal refining and forming

activities); Zip Fasteners; General Engineering (Yorkshire

Imperial Alloys, Eley, IMI Components etc.); Special Purpose

Valves (Mapegaz, Mecafrance, IMI Bailey Valves, Samuel

Birkett, CCI etc.); Heat Exchange (IMI Marston, IMI Radiators

etc. and initially the drinks dispense activities); Building

Products (YIM, YIP, etc); Fluid Power (Enots, Norgren

etc.); and, from 1982, Drinks Dispense (Cornelius, Paxman,

Redditch Controls etc.)

1980

Two workers are killed at the Summerfield rocket research

station, operated by the Company.

Company sales are down by 5% overall. IMI Titanium announces

a multi-million pound expansion at Witton (melting and

forging) and in South Wales (rolling). The performance

of the Kirkby tube factory has improved significantly

and further major investment is sanctioned. But the Board

declines to make further investment in more modern rolling

mills and so the fate of IMI Rolled Products is effectively sealed. The manufacture of copper semis

is in any case dwindling and now represents only a small

part of the Company's activity. IMI Rod and Wire is sold

to McKechnie.

is effectively sealed. The manufacture of copper semis

is in any case dwindling and now represents only a small

part of the Company's activity. IMI Rod and Wire is sold

to McKechnie.

The decline in the zip fastener business leads the Company

to write off its equity interest, although the activity

does of course continue. IMI Components and Eley are contracting.

IMI Titanium (right)

is having a second very difficult year with a collapse

in demand. But the Drinks Dispense business is thriving

and the Fluid Power activities show signs of recovery.

One

in seven of the Company's 24,500 employees lose their

jobs this year due to the general slump and the need for

cost cutting.

Collaboration between the Company and BTR is discussed

and the latter take a 25% stake in IMI Marston whilst

their Palmer Aero Products business is acquired and relocated

to Wolverhampton; Marston's name is changed, temporarily,

to Marston Palmer.

1981

The recession continues to bite

and total sales are down by a further 10%. IMI Enots,

IMI Norgren Shipston and IMI Pneumatics are merged into a single company, IMI Norgren Enots. Control

Components International of California (control valves)

is bought (shown

right in 1986).

About 40% of the Company's production is now carried out

abroad and of the UK production 20% is exported. It is

still felt that further independence from the U.K. economy

is needed.

merged into a single company, IMI Norgren Enots. Control

Components International of California (control valves)

is bought (shown

right in 1986).

About 40% of the Company's production is now carried out

abroad and of the UK production 20% is exported. It is

still felt that further independence from the U.K. economy

is needed.

Princess Margaret visits Witton in December.

1982

The dividend to shareholders is

reduced. The whole of Cornelius is acquired and becomes

IMI Cornelius. In two years IMI has become one of the

world's largest suppliers of drinks dispensing equipment.

1983

There is launched a collaborative scheme between IMI and

Birmingham City Council and using half of IMI's 228 acre

Witton site to provide an eventual 2m. sq.ft. of industrial

space in modern buildings. Turnover is £676m. and profit

£31m. £20m. has been spent over the last four years on

reorganisation and redundancy. IMI's employees now total

15,485, just 60% of the level four years previously.

1984 Development of the Holford

site begins which will lead to the creation of an award

winning industrial estate. Not everything being swept

away will be a dismal industrial  landscape:

it will include the more picturesque corner occupied by

Holford House (left).

landscape:

it will include the more picturesque corner occupied by

Holford House (left).

Drinks Dispense is contributing 30% of the profits from

only 15% of the turnover. Fluid Power is also doing well.

Elkington Copper Refiners of Walsall is acquired and the

activity absorbed into James Bridge Works. There is a

management buyout of IMI Wilkinson and J. F. Ratcliff

(Metals). Rolled Metals is now the Company's only copper

and brass semi activity at Kynoch Works and represents

a mere 3% of turnover. BTR and IMI merge their radiator

service and distribution businesses under the name International

Radiator Services. Pactrol Electronics (energy saving

controls) is acquired. Eley ammunition accounts for 15

out of a possible 24 medals at the Los Angeles Olympics.

1985

Henry Righton & Co. is sold

to Granges. Sales of rolled metals fall by 10%. The new

product area of Drinks Dispense is faltering slightly

this year but Fluid Power and Special Purpose Valves show

improved profit. The titanium business is performing well;

provisional agreement is reached whereby Sumitomo of Japan

will take a 50% stake in IMI Titanium but is shelved when

profitability declines. Discussions also occur with US

manufacturers with the aim of licensing IMI's technology

but again these come to nothing. Yorkshire Imperial Plastics

is experiencing difficult trading conditions and the Wrexham

factory closes. IMI Marstair expands and following its

acquisition of I.S. Air Conditioning becomes IMI Air Conditioning.

The precision diecasting activity of IMI Components is

an early occupant of premises on the new Holford trading

estate. A second phase is sanctioned.

1986

Martonair

International is acquired at a cost of £88m, the

biggest acquisition to date. This transforms IMI's Fluid

Power Group into

one of the world's largest manufacturers of pneumatic

equipment, matching the Company's position in the field

of drinks dispensing. The acquisition of Webber

Electro Components plc (pneumatic

solenoids) and, next year, of the Swedish AB Westin &

Backlund's pneumatic division will further strengthen

this area of activity. Coldflow (drinks dispensing equipment)

is purchased and added to the Drinks Dispense group of

companies.

Significant further investment in the tube business at

Kirkby (right)

is sanctioned and the capillary fittings business of Glynwed

Tubes and Fittings is acquired.

233,000 sq.ft. of space on the Holford trading estate

(a

glimpse of whose future is shown below)

have been let.

Formed in 1983, IMI Computing (software and technical

services) is now making a significant contribution to

company profitability.

1987

The Company's structure is adjusted

with each of the groups becoming the responsibility of

a specific director and being based more on market and

business areas than on products. Fluid Control now includes

valves and the heat exchange activities are grouped within

Special Engineering (formerly General Engineering) whilst

alloy tube becomes part of Refined and Wrought Metals.

The seven groups have now become five.

The company disposes of its 60% interest in Anderson Greenwood

(Australia) Pty. Ltd., its 50% holding in Silverton Engineering

Holdings (Pty.) Ltd. of South Africa (automotive radiators

and number plates), and, after a declining  performance,

its share of Mapegaz-Remati S.A. Ownership of IMI Summerfield,

which IMI is contracted to manage, passes from Royal Ordinance

to British Aeropace. Hayes Metals is sold.

performance,

its share of Mapegaz-Remati S.A. Ownership of IMI Summerfield,

which IMI is contracted to manage, passes from Royal Ordinance

to British Aeropace. Hayes Metals is sold.

The Prime Minister, Margaret Thatcher, visits Witton.

1988

CEDISA of Spain (valves and cylinders) and Martonair Belgium

are added to Fluid Power. Lintra

Lineartransporter of Stuttgart (rodless cylinders) is

also acquired as well as another manufacturer of similar

products, C&C Manufacturing of Illinois. Various distribution

companies in Europe and elsewhere are

acquired at around this time.

IMI Mouldings, which includes the Opella operation, is

sold.

Also sold is Yorkshire Imperial Plastics in the

Building Group; to the latter are however added this year

R. Woeste of Germany and Raccord Orleanais of France (both

copper fittings), in line with the strategy to make this

business more European based.

Specialised

Engineering is strengthened by a major acquisition, that

of the Conax Buffalo Corporation (temperature sensors).

Marston's

flexible fuel tank business is sold.

The 40-year

arrangement by which the Company manages the Summerfield

rocket motor establishment is terminated.

Eley

and IMI Titanium are both recipients of the Queen's Award

for Technological Achievement.

1989

During

this period Drinks Dispense is enjoying good business

in Europe but the situation is less happy in North America.

Attempts to improve this include the concentration of

Cornelius's component production in a single plant at

San Antonio, Texas and the reaching of a world-wide supply

agreement with Coca-Cola. In

the Americas the Company now has manufacturing plants

in Brazil and Canada, in addition to the USA and several

European countries. Markets for drinks dispense products

are being developed also in China, Taiwan, the Philippines

and Indonesia. Similar progress is being made by the Cannon

service equipment group and several acquisitions are made

in this period, including Cumberland Corporation, (mobile

merchandising carts and milk cases). In this year Cannon

obtains its first contract for an automated cold storage

system for dairy products for a major UK supermarket chain.

In Refined and Wrought Metals, IMI Titanium is performing

well. The acquisition of TiTech International (titanium

castings) gives it a long-sought presence in North America. In the rest of

the Group, the emphasis is not on growth but on the most

effective use of the asset base as, in the case of IMI

Rolled Metals, Yorkshire Imperial Alloys and possibly

the refining companies (right),

the business declines.

a long-sought presence in North America. In the rest of

the Group, the emphasis is not on growth but on the most

effective use of the asset base as, in the case of IMI

Rolled Metals, Yorkshire Imperial Alloys and possibly

the refining companies (right),

the business declines.

Special Engineering sees this year a major disposal, that

of IMI Radiators to Nippondenso.

In the Building Group IMI Pacific of France (cylinders)

is disposed of.

Holford Estates continues to progress well: 640,000sq.ft.

has been built or reserved and over 1350 jobs created.

Its book value is put at £18.7m.

Sales reach £1bn. for the first time.

The

1990s

This decade will see initially a return to recession for

the first three years, followed by a recovery for the

rest of period. It will be marked for the Company by significant

restructuring and an acceleration in corporate activity;

and it will witness the final departure from the traditional

metal smelting, metal founding and construction-related

business as expansion of the newer core businesses gathers

momentum.

1990

IMI decides to abandon the rolled metals industry. In

Drinks Dispense, MK Refrigeration Group (drinks cooling

equipment and

optics- see right) and Conveyor Speciality

Systems of Minnesota (material handling

equipment), later renamed Cannon Conveyor Systems, are

acquired as well as two small distributors in Greece and

Italy. Brook Street Computers is purchased .

1990

IMI decides to abandon the rolled metals industry. In

Drinks Dispense, MK Refrigeration Group (drinks cooling

equipment and

optics- see right) and Conveyor Speciality

Systems of Minnesota (material handling

equipment), later renamed Cannon Conveyor Systems, are

acquired as well as two small distributors in Greece and

Italy. Brook Street Computers is purchased .

1991

IMI Rolled Metals is closed and plant sold off.

The closure process takes much of the year and runs smoothly,

a tribute to good industrial relations and cooperation.

Thus ends the Company's association with an activity which

dates back to 1877 and has involved thousands of Birmingham

working people over 114 years.

IMI buys the Birmingham Mint Ltd. of Icknield Street.

The IMI Birmingham Mint Ltd. is formed and all minting

operations are transferred from Kynoch Works to Icknield

Street. The Company also acquires A.W. Cash Valve, an

American producer of heating and plumbing controls, and

Remcor Products of Chicago (ice/drink combination machines);

the latter acquisition brings a strengthening of Drinks

Dispense Group's association with Coca Cola. IMI Titanium's

profitability slumps dramatically due to market conditions

as does that of Yorkshire Imperial Alloys, a situation

from which the latter will not recover.

Redwood International (software) is acquired, bringing

IMI 's annual computing sales up to £50m.

1992

The Building Products group continues

to decline, being hit especially hard this year, its sales

reducing for the third consecutive year, from £404 million

in 1989 to £305 million with a corresponding hit on profits.

IMI's Special Engineering profits also decline dramatically.

The Refined and Wrought Metals Group disappears and the

remaining businesses now fall under Special Engineering

and Building Products. Walter AG, Switzerland's leading

manufacturer of valves, cylinders and air service units

is acquired to strengthen Fluid Power. But the trading difficulties faced by that group force

a move towards the rationalisation of its worldwide manufacturing

operations: thirty locations will in due course be reduced

to twelve. Marston's aircraft engine ring business (left)

is sold to an American competitor.

But the trading difficulties faced by that group force

a move towards the rationalisation of its worldwide manufacturing

operations: thirty locations will in due course be reduced

to twelve. Marston's aircraft engine ring business (left)

is sold to an American competitor.

1993

The Company's four main areas of activity continue to

be: Building Products, Fluid Power, Drinks Dispense and

Special Engineering.

Fluid Power's profitability dips this year, prior to significant

improvement in the following years as the effect of restructuring

is felt. Within the Building Group however the performance

is sharply improved following major investment in the

tube and refining activities. Contrary to previous policy

the Board now decides to consider the possibility of acquiring

a plastics activity.

In Drinks Dispense, Cornelius is appointed a preferred

supplier to Coca Cola. Relationships with Pepsi are however

not soured and a strategic alliance will be agreed between

the two companies early next year.

The performance of Specialised Engineering is adversely

affected by IMI Titanium's problems in a difficult market

and the Company opens discussions with Timet of the USA

about possible cooperation. Casino Tokens Inc. of Las

Vegas is acquired to supplement the minting operation.

1994

37 acres of surplus land at Witton is sold, as well as

Phase 1 of the Holford Industrial Estate (right)

which nets £24m. Brook Street Computers and Redwood

International are sold following operating losses. IMI

Range and IMI Stanton merge. Andrews Water Heaters is

bought. Within Specialised Engineering, IMI Titanium's

losses double to £7m. despite a 30% increase in

sales. Yorkshire Imperial Alloys is also having difficulties,

faced with similar problems: international over-capacity

and uncompetitive plant and equipment.

1994

37 acres of surplus land at Witton is sold, as well as

Phase 1 of the Holford Industrial Estate (right)

which nets £24m. Brook Street Computers and Redwood

International are sold following operating losses. IMI

Range and IMI Stanton merge. Andrews Water Heaters is

bought. Within Specialised Engineering, IMI Titanium's

losses double to £7m. despite a 30% increase in

sales. Yorkshire Imperial Alloys is also having difficulties,

faced with similar problems: international over-capacity

and uncompetitive plant and equipment.

1995

There is a major reorganisation of IMI Titanium involving

substantial redundancies which returns the activity to

profit and the discussions with Timet about a possible

joint venture reach a satisfactory conclusion. It is announced

that the Company's titanium interests are to be merged

with those of Tremont Corp. of the U.S.A., the owner of

Timet, giving IMI a 38% stake in the new company. The

possible disposal of Yorkshire Imperial Alloys is actively

pursued. Elsewhere in the Specialised Engineering Group,

special purpose valves and IMI Components are doing well.

In Building Products, IMI Waterheating, a merger of Santon

and Range, is having trading difficulties and a decision

is made to close two factories. Similar difficulties at

IMI Cash Valve (formerly A.W. Cash Valve) lead to a transfer of the business from Illinois to Alabama.

There are also

lead to a transfer of the business from Illinois to Alabama.

There are also significant site configuration changes in the French,

Belgian and Hungarian operations. In September is announced

the Company's biggest ever (£134m.) acquisition,

that of Heimeier, the largest manufacturer of thermostatic

radiator valves in Germany (whose Erwitte factory

is shown above and typical product right).

significant site configuration changes in the French,

Belgian and Hungarian operations. In September is announced

the Company's biggest ever (£134m.) acquisition,

that of Heimeier, the largest manufacturer of thermostatic

radiator valves in Germany (whose Erwitte factory

is shown above and typical product right).

Bar-Master International (bar valve dispense equipment)

is added to Drinks Dispense.

1996

In February the Timet transaction is completed. In April

the Company seizes an opportunity to sell its holding

in Timet and thus at £105m. completes its withdrawal

from titanium on better terms than might previously been

envisaged. Almost the whole of the titanium interests

are sold, as is IMI Computing, the subject of a management

buy-out. Purchases include the American businesses of

Mosier (pneumatic actuators) and ISI Automation (pneumatic

components - £84m.) which are added to the Fluid

Power group. A wholly new factory is commissioned in China

to manufacture drinks dispense equipment and Objex Ltd.

(countermount displays) is acquired. 50% of IMI's employees

are now resident outside the U.K.

1997

The policy of divesting non-core businesses continues.

Conax Buffalo is sold (£4.4m.) After unsuccessful

attempts at disposal IMI Yorkshire Alloys is closed following

unacceptable

losses. There are more acquisitions: TA Hydronics of Sweden

(hydronic balancing valves - £93m. - see left) and

Herion, Germany (hydraulic components - £39m.),

both for Fluid Power; and Sulzer's industrial valve division,

Thermtec, for Specialised Engineering. A decision is made

to rationalise the global manufacturing facilities of

Drinks Dispense: this will result in manufacturing units

reducing from 20 to 14 and a new factory to manufacture

beer coolers at Brighouse where Paxman had started to

make them thirty years earlier.

unacceptable

losses. There are more acquisitions: TA Hydronics of Sweden

(hydronic balancing valves - £93m. - see left) and

Herion, Germany (hydraulic components - £39m.),

both for Fluid Power; and Sulzer's industrial valve division,

Thermtec, for Specialised Engineering. A decision is made

to rationalise the global manufacturing facilities of

Drinks Dispense: this will result in manufacturing units

reducing from 20 to 14 and a new factory to manufacture

beer coolers at Brighouse where Paxman had started to

make them thirty years earlier.

The 30% stake in International Radiator Services, formed

with BTR in 1984, is sold.

1998

The disposal of those businesses which have no obvious place in the Company's strategy continues: the Birmingham

Mint Group (£18m.), IMI Waterheating (£20m.),

IMI Pactrol (£10m.), Marston's industrial heat exchanger

business (£21m.), IMI Precision Diecastings and

IMI Reeves. Wilshire Corporation of Illinois (air conditioning

and refrigeration - see right) is acquired for Drinks

Dispense and supplements Cornelius's activities; and KIP

Inc. of Connecticut (solenoid valves - £18m.) for

Fluid Power. The four main areas of activity remain but

as the activities become more concentrated Building Products

is now known as Hydronic Controls and Specialised Engineering

as Energy Controls, reflecting its increasing focus.

place in the Company's strategy continues: the Birmingham

Mint Group (£18m.), IMI Waterheating (£20m.),

IMI Pactrol (£10m.), Marston's industrial heat exchanger

business (£21m.), IMI Precision Diecastings and

IMI Reeves. Wilshire Corporation of Illinois (air conditioning

and refrigeration - see right) is acquired for Drinks

Dispense and supplements Cornelius's activities; and KIP

Inc. of Connecticut (solenoid valves - £18m.) for

Fluid Power. The four main areas of activity remain but

as the activities become more concentrated Building Products

is now known as Hydronic Controls and Specialised Engineering

as Energy Controls, reflecting its increasing focus.

1999

A view on the increasing trend in the European building

sector towards plastics and away from traditional materials

leads to the purchase (£350m.) of Polypipe, a manufacturer

of plastic drainage products (left). This

trend also threatens other companies in the Hydronics

Controls Group and all of them are operating under generally

difficult trading conditions. The refining activities

are badly hit by this and by new environmental regulations

and the Company feels compelled to withdraw from all activities

in that area apart from billet casting, a move which leads

to extensive redundancies.

1999

A view on the increasing trend in the European building

sector towards plastics and away from traditional materials

leads to the purchase (£350m.) of Polypipe, a manufacturer

of plastic drainage products (left). This

trend also threatens other companies in the Hydronics

Controls Group and all of them are operating under generally

difficult trading conditions. The refining activities

are badly hit by this and by new environmental regulations

and the Company feels compelled to withdraw from all activities

in that area apart from billet casting, a move which leads

to extensive redundancies.

Drinks Dispense acquires a US company, Jet Spray, which

takes the Company into hot drink dispensing for the first

time and opens new areas of business opportunity. Also

acquired is Melrose Displays Inc. of New Jersey (point-of-purchase

displays- £4.9m.)

The last of Marston's major activities, its aerospace

interests, are finally sold to a US company, Hamilton

Standard, a United Technologies subsidiary (£16.6m.)

and the new company is called HS Marston. Just two small

activities remain: heat sinks which will later be absorbed

into HS Marston and bursting discs which will become part

of IMI Safety Systems. And so the Company's almost eighty

year association with Marston - whose own roots in Midlands

industry are even deeper than those of Kynoch and stretch

back to 1740 - is severed.

Energy Controls now comprises exclusively controls companies

with the exception of the Witton based nuclear components

and ammunition operations.

The

2000s

An even greater concentration on what are seen as the

Company's core businesses will be seen in this decade.

Almost every "traditional" business will disappear and

the Company will be transformed beyond recognition.

2000

A detailed review of the Company's businesses is in hand.

Employees now total 19,000 worldwide. Flow Controls Inc., USA is

acquired.

now total 19,000 worldwide. Flow Controls Inc., USA is

acquired.

2001

The Company's future strategy is revealed. Concentration

will be on the business areas of Fluid Controls and Retail

Dispense which provide five discrete business segments

serving large, market-leading customers.

The Fluid Controls businesses operate in the area of power

generation and oil and gas (Severe Service); essential

pneumatic systems for automotive, medical and other outlets

(Fluid Power); and energy conservation and personal comfort

in buildings (Indoor Climate).

The Retail Dispense businesses service major drinks producers

and retailers (Drinks Dispense); and producers and retailers

of other branded items at point of display (Merchandising

Systems).

The Company is moving into high value, knowledge based

engineering and systems based-solutions. The cost base

will be reduced and some manufacture will be outsourced

or moved to low cost areas of the world including Mexico,

China and Eastern Europe. 30% of existing manufacture

will be affected over the next two years. Manufacturing

capacity in China is doubled. Two new facilities are created

in Mexico.

Various traditional businesses in the old Building Products

Group have no place in this new strategy.

2002

The Copper Fittings and Copper Tube businesses are sold.

The Eley ammunition business is sold too, the activity

out of which the company has grown, which has survived

for almost a century and a half and to which the origins

of the newer businesses can all be traced. Cartridge manufacture

will move to Minworth.

Acquisitions include STI Milan and DCI Milwaukee (point-of-sale

services).

The streamlining of administration costs has led to job

losses and a significant reduction in people costs.

The remainder of the Witton site is sold for redevelopment

but IMI's Severe Service business will stay on the site,

in leased premises.

A new history of the Company is published: "A World

of Engineering - The Story of IMI 1862- 2001" by

Ewan Fraser and John Metcalf.

2003

Artform International Ltd., Loughborough (a point-of-sale

equipment provider), Commtech, U.K., (indoor climate commissioning

and servicing) and Fluid Kinetics, California (industrial

silencers) are acquired.

In April the Kynoch Works site is vacated after 141 years.

The new IMI Headquarters is an office block at Lakeside,

on the Birmingham Business Park at Solihull and convenient

for the airport.

2005

Polypipe is sold. This disposal marks the end of the portfolio

repositioning announced in 2001 and the Company has now

been transformed to a greater extent than at any other

time in its long history. The aim is announced of raising

the proportion of total production in low cost economies

from the present 25% to 40%. Company turnover is now £1.3bn.

The present location of the approx. 14,000 employees is

as follows: UK - 2700, Europe - 5000,

Americas - 5300, Asia - 1000 and Elsewhere - 100.

2006

Truflo, a US manufacturer of pumps, is acquired in April

(£113m) and becomes part of the Fluid Controls Group.

The Company's residual responsibility for the copper fittings

business, sold in 2002, leads to its liability for a European Commission fine of 48.3m. euros against which it appeals.

New products include new control valve and strainer products

for the natural gas and nuclear industries; a

device to protect agains legionella in cooling systems;

and merchandising products for Microsoft's new Zune music

and digital player. The trend towards increased manufacture

in lower cost economies continues. The

Company's newest overseas facility, the Cornelius plant

in the Ukraine, begins production this year. Major operational

locations are now: Austria, China, Czech Republic

(see

right, Norgren's Brno plant),

Germany, Italy, Japan, Mexico, South Korea, Sweden, Switzerland,

UK, Ukraine and USA.

Commission fine of 48.3m. euros against which it appeals.

New products include new control valve and strainer products

for the natural gas and nuclear industries; a

device to protect agains legionella in cooling systems;

and merchandising products for Microsoft's new Zune music

and digital player. The trend towards increased manufacture

in lower cost economies continues. The

Company's newest overseas facility, the Cornelius plant

in the Ukraine, begins production this year. Major operational

locations are now: Austria, China, Czech Republic

(see

right, Norgren's Brno plant),

Germany, Italy, Japan, Mexico, South Korea, Sweden, Switzerland,

UK, Ukraine and USA.

Within the Fluid Controls group, the key businesses are:

CCI, Truf lo Rona and Orton (Severe Service); Norgren

(Fluid Power); and TA, Heimeier and FDI (Indoor Climate).

Within Retail Dispense they are: Cornelius and 3Wire (Beverage

Dispense); and Cannon, DCI Marketing, Artform and Display

Technologies (Merchandising Systems).

2007

2007

The company grows by nearly 7% and

achieves revenue of £1,599m. and an increase in

profitability of 10%. 14700 people are directly employed

throughout the world. The overall strategy - focus on

leading customers in niche markets to whom bespoke and

innovative solutions can be provided and whose growth

the Company can share, reinforced by effective account

management and after-sales service - is unchanged and

continues to be pursued vigorously.

Kloehn (specialist fluid handling systems in the life

science sector - £30m.) and Pneumatex (water conditioning

equipment - £19m.) are acquired this year.

The trend towards the transfer of more manufacturing facilities

to lower cost economies continues. The manufacturing operation

for merchandising equipment in China has trebled and that

for Fluid Power  in

Mexico doubled.

in

Mexico doubled.

These are the business areas:

- Severe Service (CCI, Orton, Truflo Rona, Newman Hattersley)

- £362m., 2400 people (above

right)

- Fluid Power (Norgren) - £571m., 6000 people

- Indoor Climate (TA, Heimeier, FDI, Pneumatex) - £207m.,

2000 people

- Beverage Dispense (Cornelius, 3Wire) - £285m., 2500

people

- Merchandising (Artform, Cannon, DCI, DT) - £174m.,

1400 people

(right)

Innovative new products this year include actuator and

valve controls for nuclear power plants; door operating

systems for Siemens high speed trains; climate control

systems for Terminal 5; new, energy-efficient refrigeration

equipment for drinks dispensing; a new cold beer station

for Coors; and new LED lighting advances for cosmetics

merchandising.

2008

The Company continues to demonstrate progress: sales are significantly increased and profits modestly so. Evidence of innovation is also apparent. Sales of new products introduced over the previous three years account for around one-seventh of turnover. Significant introductions include new wellhead gas production chokes, several new valve types for the life sciences sector, and 'Viper', a new frozen beverage dispenser. The year sees the completion of a three-year programme to transfer a greater proportion of production capacity to low cost economies. By the end of the year the global recession is starting to make itself felt generally on the Company's business and with particular effect on those parts of the Company dependent on the automotive, commercial vehicle, construction and soft drinks bottling industries.

2009

The early part of the year sees the need for significant retrenchment in the face of the downturn. The global workforce is reduced by about 17% (2600 people) and extensive short-time working introduced. Further production capacity is moved out of Europe and North America. A new Fluid Power facility is opened in Shanghai and rapid progress is made on two new Severe Service facilities, at Brno and Chennai. The current manufacturing activity in low-cost countries is likely to increase from 35% of the total to about 50% over the next 2/3 years. All these measures, together with significant investment in emerging markets and new product development, ensure a continuing healthy financial position for the Company despite all the difficulties in the marketplace. Successful new products include a new high performance differential pressure control valve for large cooling systems and district heating systems (Indoor Climate) and an integrated pneumatic system to control gas in anaesthesia ventilators (Fluid Power). The prospects for 2010 are marginally improved.

2010

Demand in many of the Company's markets has increased and the financial results indicate a strong performance. The Company's concentration is on maintaining technology leadership in the precise control of fluids in critical applications; market leadership in global niches populated by large successful customers; and high exposure to key global trends driving economic growth.

In the Severe Service valve business the new manufacturing facility in the Czech Republic opens in May and its sister facility in India is also operational; the Oil & Gas and LNG sectors are recovering strongly whilst business in the Fossil Power and Nuclear sectors are quiet; agreement is reached to create a new venture to supply control valves into the China nuclear industry.

The Fluid Power business is busy in its five key global sectors -- Commercial Vehicles, Life Sciences, Rail, Energy and Food & Beverage; manufacturing continues to be transferred to the Company's low-cost facilities in China, the Czech Republic, Brazil and Mexico.

The Indoor Climate business returns to growth; the engineering and sales resource is being expanded, especially in the emerging markets and North America.

In Beverage Dispense recovery is also continuing; the strongest markets are the Americas and China; new product development targets the higher growth water, juice, frozen drinks and smoothies markets; demand for the new more energy-efficient coolers is also growing.

In the Merchandising business some growth is also seen, especially in the automotive sector; plans are in hand to open a new "In-Vision" Centre in the USA to explain the science of merchandising to customers and demonstrate how the Company can add greater value for them.

2011

Further improvements in performance are seen, greatly assisted by the Company's market leading technology in many of its global niche markets.

The Severe Service valve business shows growth assisted by the results of the newly acquired Zimmerman & Jansen and TH Jansen; the acquisition of Remosa sPa and Grupo InterAtiva in Brazil strengthen isolation valve capabilities.

In Fluid Power manufacturing continues to be transferred to low cost sites in China, the Czech Republic and Mexico.

The Indoor Climate business currently relies significantly on refurbishment projects, reflecting the subdued new construction market in Europe; investment continues to be made in educating the market to help drive demand and some 83,000 customers attend one of the Company's seminars, especially in North America, Germany and China; a new range of balancing and control valves is being developed and centres have opened to demonstrate hydronic control involving the recruitment of 50 more hydronic sales engineers.

The strongest markets for Beverage Dispense is the Americas; several major new product development opportunities have been identified.

In Merchandising a large automotive project is completed and that sector shows signs of improvement with dealers once again investing in their showrooms; the InVision retail science laboratory is opened in Milwaukee, USA: this state-of-the-art facility enables customers to see how the Company can assist them to further their own business.

2012

There is another encouraging financial performance with a small overall growth and an improvement in operating margins. The company's strategy is to concentrate on areas where its fluid technologies can best be used in global market niches leading to a leadership position and heightened exposure to long-term trends of climate change, resource scarcity, urbanisation and an ageing population.

The logic of this strategy leads to the conclusion that the majority of the Merchandising business should be divested and options are being explored. A part of this business which offers certain synergies is transferred to the Beverage Dispense activity.

The Severe Service valve business grows especially in Fossil Power and Oil & Gas, as does Merchandising.

Fluid Power, Indoor Climate and Beverage Dispense all have a more difficult year with overall revenues flat or declining slightly but with an overall improvement in profitability.

This is a summary of the current Company activities, on the 150th anniversary of the day when a young George Kynoch trundled a shed on rollers from central Birmingham to establish his percussion cap business in the hamlet of Witton:

SEVERE SERVICE

Activity: highly engineered valves and controls, used in critical applications and extreme operating environments, enabling vital industrial and energy production processes to operate safely, cleanly and more efficiently.

Key brands: CCI, BTG, IMI Nuclear, Orton, Truflo Rona, STI, Z&J, THJ, Remosa, InterAtiva.

Main markets: fossil power; nuclear power; liquefied natural gas; iron and steel; petrochemical and refining.

Major operational locations: Belgium, Brazil, China, Czech Republic, Germany, Italy, Japan, South Korea, Sweden, Switzerland, UK and USA.

Employees: 4350

FLUID POWER

Activity: specialists in motion and fluid control technologies, both pneumatic and electric, custom engineered for critical applications requiring precision, speed and reliability.

Key brands: Norgren, FAS, Kloehn, Herion, Buschjost, Maxseal

Main markets: commercial vehicles; food and beverage; life sciences; rail; energy and industrial pneumatic applications.

Major operational locations: Brazil, China, Czech Republic, Germany, Mexico, Switzerland, UK and the USA

Employees: 5950

INDOOR CLIMATE

Activity: experts in hydronic distribution systems and room temperature control which deliver optimal and energy efficient indoor climate systems.

Key brands: TA Hydronics, Heimeier, Pneumatex, FDI

Main markets: water-based heating; cooling systems for commercial buildings; and temperature control for residential buildings.

Major operational locations: Germany, Poland, Sweden, Switzerland and USA.

Employees: 1950

BEVERAGE DISPENSE

Activity: specialists in innovative beverage cooling and dispense solutions that contribute to increased sales and lower operating costs.

Key brands:Cornelius, 3Wire .

Main markets: cooling for soft drinks; health and wellness drinks and alcoholic beverages; and dispense and point of sale equipment for bars, restaurants and retail outlets.

Major operational locations: China, Germany, Mexico, UK and the USA.

Employees: 2250

MERCHANDISING

Activity: specialists in bespoke a permanent point of sale merchandising solutions and technologies which improve retailer and brand owner profitability by driving impulse purchase.

Key brands: Artform, Cannon Equipment, DCI Marketing, Display Technologies..

Main markets: global brand owners and retail sales outlets.

Major operational locations: UK and USA.

Employees: 850

2013

A reshaping of the business takes place. The

Beverage Dispense and Merchandising divisions are

disposed of (to the Marmion Group for £690m; and £620m

is returned to shareholders). The Company is now a

specialist flow control business, focused entirely on

industrial end markets. Martin Lamb, Chief Executive for

13 years, retires; in that period the Company has

transformed itself into a leading specialist engineering

business. The new Chief Executive initiates a major

review of the Company's markets, capabilities, scope for

improved Group coordination and possibilities for future

investment.

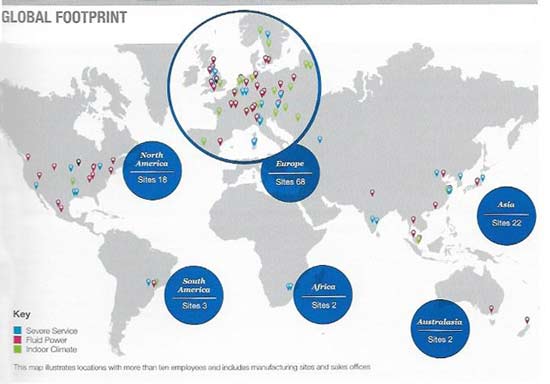

The

Company now operates as three divisions:

Severe Service;

Fluid Power; and

Indoor Climate. The key

brands, main markets and major operational locations

remain essentially as in 2012. (Those for the Beverage

Dispense and Merchandising divisions have disappeared

from the Company's portfolio). This is the Company's

current Global Footprint showing 93 different sites

(right).

The

Company now operates as three divisions:

Severe Service;

Fluid Power; and

Indoor Climate. The key

brands, main markets and major operational locations

remain essentially as in 2012. (Those for the Beverage

Dispense and Merchandising divisions have disappeared

from the Company's portfolio). This is the Company's

current Global Footprint showing 93 different sites

(right).

Revenue for the Company is now £1743m (+3% over last

year) and profit before tax £297.7m (+8%).

2014

The review of activities identifies the need for greater

investment in product development; better Company-wide

collaboration and coordination (IT systems and

facilities); improved organisational structure; greater

concentration on those existing markets where the

greatest potential for growth and profit exists; and an

expansion, via acquisition, of addressable markets.

The Company's three divisions are now known as:

-

IMI Critical Engineering

(previously Severe Service), comprising 14 companies

operating in 12 countries.

-

IMI Precision Engineering (previously Fluid

Power), comprising 5 companies with manufacturing

facilities in 8 countries and a presence in 75.

-

IMI Hydronic Engineering

(previously Indoor Climate), comprising 4 companies

manufacturing in 6 countries

In the course of the

year the IMI Components manufacturing site in Birmingham

is closed following a drop in demand in the nuclear fuel

enrichment market; and the Eley businesses are sold for

£42m. Bopp & Reuther, the German power generation valve

specialist, is acquired for £153m. and becomes part of

the Critical Engineering Division.

Revenue for 2014 is £1686m and profit

£278.1m.

One of Critical Engineering's

impressive products:

2015

Worldwide economic conditions are difficult, with

special problems in China and Brazil. This affects

the Company's activities and performance. Some

contraction of manufacturing capacity is made, although

Critical Engineering complete three larger manufacturing

sites in Houston, Italy and Korea (the latter for IMI

CCI at a cost of £8m and pictured left). Company revenue

for the year is £1557m. (-5%) and profit £218.7m.

(-21%).

Worldwide economic conditions are difficult, with

special problems in China and Brazil. This affects

the Company's activities and performance. Some

contraction of manufacturing capacity is made, although

Critical Engineering complete three larger manufacturing

sites in Houston, Italy and Korea (the latter for IMI

CCI at a cost of £8m and pictured left). Company revenue

for the year is £1557m. (-5%) and profit £218.7m.

(-21%).

New

data management, project management and

quality systems

are being introduced throughout the divisions. This is

an ongoing plan and will continue for a long period,

across all the sites. R&D expenditure is increasing,

currently 3% of revenue with the target of 5% by 2017.

Critical Engineering have successfully integrated Bopp &

Reuther into their activities. New products are

introduced, especially in Hydronic Engineering where

some 29 have appeared since 2014. They include

"Eclipse", a next-generation automatic thermostatic

radiator valve which sells 500,000 units in the first

five months after introduction, compared with 100,000 by

its predecessor throughout its entire product life.

Precision Engineering are working on a new Industrial

Automation product range to be introduced in late 2016.

quality systems

are being introduced throughout the divisions. This is

an ongoing plan and will continue for a long period,

across all the sites. R&D expenditure is increasing,

currently 3% of revenue with the target of 5% by 2017.

Critical Engineering have successfully integrated Bopp &

Reuther into their activities. New products are

introduced, especially in Hydronic Engineering where

some 29 have appeared since 2014. They include

"Eclipse", a next-generation automatic thermostatic

radiator valve which sells 500,000 units in the first

five months after introduction, compared with 100,000 by

its predecessor throughout its entire product life.

Precision Engineering are working on a new Industrial

Automation product range to be introduced in late 2016.

IMI Scott and IMI Z&J South Africa are disposed

of as non-core businesses.

Here

(right)

is a batch of IMI CCI control valves at C.E.'s site in

the Czech Republic.

2016

Market conditions remain tough but results

are in accordance with expectations: revenue £1649m.

(-5%) and profit £208m. (-5%). Because of these market

difficulties, eight, lower growth and higher cost Critical

Engineering sites have been sold or closed and

othercost-cutting measures have been adopted throughout

the Company. In C.E a loss-making Italian service

business is sold. However, confidence in the plans to

develop the business remains strong.

This is a

summary of the market sectors in which the three

divisions are active and the products supplied:

CRITICAL ENGINEERING:

Power

Generation (turbine bypass valves);

Oil and Gas

(anti-surge valve and actuator systems for LNG

compression facilities); Petrochemical (integrated flow

control systems in Fluid Catalytic Cracking, bespoke

valves for ethylene, polypropylene and delayed coking

production processes); Actuation (complete actuation

systems to operate industrial valves for demanding

applications and processes).

PRECISION

ENGINEERING:

Industrial Automation (high

performance valves, valve islands, proportional and

pressure monitoring controls, air preparation products

and pneumatic actuators); Commercial Vehicle (chassis

and powertrain solutions which deliver fuel efficiency,

emissions reduction and faster assembly times for

commercial vehicle manufacturers);

Oil and Gas (harsh

environment precision control products including

stainless steel valves and regulators, nuclear class

valves and emergency shutdown controls);

Life Sciences

(precision flow control solutions used in medical

devices, diagnostic equipment and biotech and analytical

instruments).

Industrial Automation (high

performance valves, valve islands, proportional and

pressure monitoring controls, air preparation products

and pneumatic actuators); Commercial Vehicle (chassis

and powertrain solutions which deliver fuel efficiency,

emissions reduction and faster assembly times for

commercial vehicle manufacturers);

Oil and Gas (harsh

environment precision control products including

stainless steel valves and regulators, nuclear class

valves and emergency shutdown controls);

Life Sciences

(precision flow control solutions used in medical

devices, diagnostic equipment and biotech and analytical

instruments).

Precision Engineering's customers now only

have to use an App if they need a repacement part in a

hurry, whether it's to repace an IMI part or a

competitor's. Scan the part no. or photograph the item and

up will come ordering details

(above left).

HYDRONIC ENGINEERING:

Balancing and Control (balancing and control systems to

keep comfort in buildings at the right level and to

increase efficiency levels); Thermostatic Control

(thermostatic control systems guaranteeing direct or

automatic control of radiators and underfloor heating

systems); Pressurisation (range of pressure maintenance

systems with compressors or pumps and expansion vessels

to maintain the correct pressure in heating, cooling and

solar systems); Water Quality (dirt and air separators

and pressure-step degassers to protect hydronic systems

by keeping water free of micro-bubbles and sludge).

2017

The Company now employs some 10647 people in over 50

countries, distributed as follows: U.K. 1265;

Continental Europe 5872; Americas 2100; Asia Pacific

1193; and Rest of the World 27. Some 160

subsidiary undertakings/Companies are listed in the

Annual Report. This is a view of the Company's new

Korean facility:

Reflecting the

international nature of IMI's business, the nationality

of the Board of Directors is currently British (3);

American and American/British (2), Australian (1);

German (1); and Danish (1). The Chairman is Lord Smith

of Kelvin and the Chief Executive, Mark Selway.

Trading conditions in the last

year have been mixed: Precision Engineering's markets

grow strongly, the Automation and Commercial vehicle

markets strengthen, the European construction markets

are slightly stronger and in North America and China

construction markets continue to grow; to offset these

movements, the Power Generation sector suffers from

lower investment and the energy market continues to be

soft. Meanwhile the Oil and Gas market starts to

stabilise. These somewhat improved conditions and also

continuing efficiency improvements (including new IT

systems throughout the organisation and the closure of

12 Critical Engineering higher-cost sites) lead to an

improved financial outcome: revenue £1751m. (+6%) and

profit £224m (+8%).

continuing efficiency improvements (including new IT

systems throughout the organisation and the closure of

12 Critical Engineering higher-cost sites) lead to an

improved financial outcome: revenue £1751m. (+6%) and

profit £224m (+8%).

Many new products are

introduced (including 13 in Hydronic Engineering) and

ambitious product development strategies are being

pursued in each of the three divisions. The Company

acquires Bimba Manufacturing, a market leading supplier

of pneumatic, hydraulic and electric motion products to

the North American Industrial Automation market, at a

cost of £138m.; it is based in Illinois. The sale of the

loss-making UK fasteners business, Stainless Steel

Fasteners, is announced. A new Critical Engineering

facility is opened in Qinpu, China

(right).

2018

As the Company enters the final year of its

Development Plan initiated in 2013, its financial

results show continuing improvement: revenue £1907m.

(+5%), profit £251m. (+12%). Trading conditions

nevertheless continue to be mixed, with, in particular,

a decline in the Fossil Power and Energy markets. UK

sales now amount to less than 5% of total revenue but nevertheless the

Company has felt it necessary to develop a number of

Brexit-related contingency plans to offset future

problems; these include increased inventories. The

Company is actively and successfully managing its

pension liabilities.

Bimba is being successfully

integrated into Precision Engineering's North American

operations and it is expected that the

introduction of various improvements in operation and

systems will lead to improvements in sales and profit.

In the same division the Indian operation

has been

relocated into a new and larger facility in New Delhi,

thus expanding its low-cost, world-class manufacturing

and engineering capability and enhancing the Company's

ability to serve its rapidly expanding market across

Asia. It is located in Noida, near New Delhi

(right). On the other hand Critical Engineering have had to

undertake several plant closures, now successfully

completed.

has been

relocated into a new and larger facility in New Delhi,

thus expanding its low-cost, world-class manufacturing

and engineering capability and enhancing the Company's

ability to serve its rapidly expanding market across

Asia. It is located in Noida, near New Delhi

(right). On the other hand Critical Engineering have had to

undertake several plant closures, now successfully

completed.

New products continue to be

introduced across the entire Group. In Hydronic

Engineering new product launches continue apace and

sales of recently introduced products now amount to 22%

of total sales in that division. This is the new

electric actuator developed by IMI Norgren which will be

launched in 2019.

Text

© staffshomeguard.co.uk 2007-2019

Images © IMI plc 2002-2019

v2.5 - 16th May 2019

STAFFS

HOME GUARD WEBSITE - MISC. INFORMATION

STAFFS

HOME GUARD WEBSITE - MISC. INFORMATION